In commercial real estate, the physical condition of a building is never just a facilities question. It is a financial question, a legal question, and a risk question — all at once. The document that ties those threads together is the Property Condition Assessment, and in markets like New Jersey and the Greater Philadelphia metro area, where aging building stock, harsh seasonal weather, and compressed transaction timelines are the norm, understanding what a PCA actually does for the parties at the table is essential.

I perform PCAs under ASTM E2018-15 standards across the NJ/PA region, and the same report I produce for a lender’s underwriting department is the same report an investor’s attorney is flagging for risk allocation language and the same report a buyer is using to decide whether to renegotiate the purchase price or walk. That cross-functional utility is what makes the PCA one of the most consequential documents produced during a commercial real estate transaction.

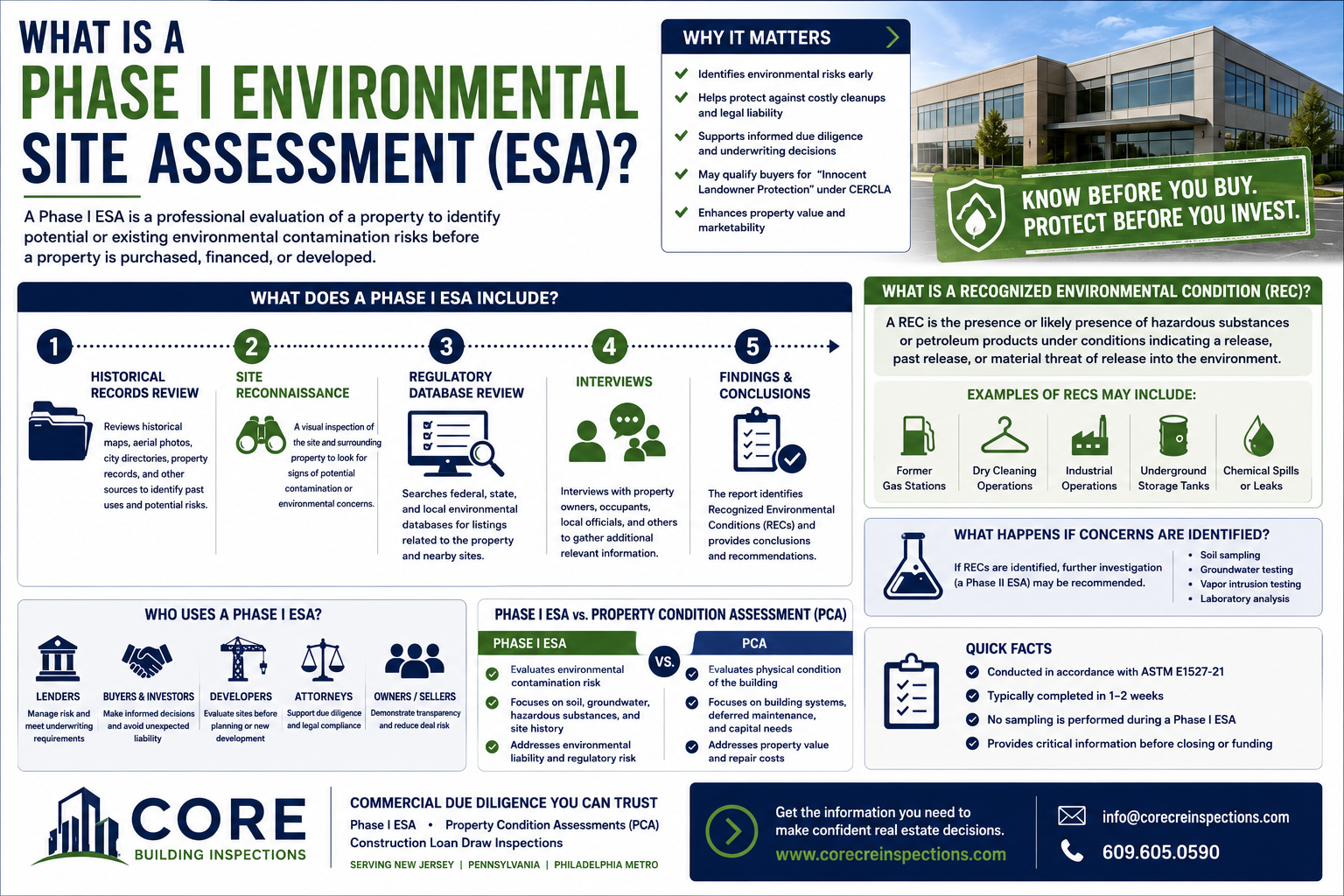

What a PCA Actually Delivers

A Property Condition Assessment is a systematic evaluation of a commercial property’s physical condition performed by a qualified practitioner. Under ASTM E2018-15 — the industry standard governing PCA scope and methodology — the assessment covers all major building systems and site improvements, documents physical deficiencies and deferred maintenance, estimates the remaining useful life of major components, and produces opinions of probable cost for both immediate repairs and longer-term capital expenditures.

The output is a structured report that translates what was observed on the ground into language that lenders, investors, and legal teams can act on. It is not a home inspection. It is not a code compliance review. It is a practitioner’s informed evaluation of how a building is performing, what it will cost to keep it performing, and where the risks are concentrated.

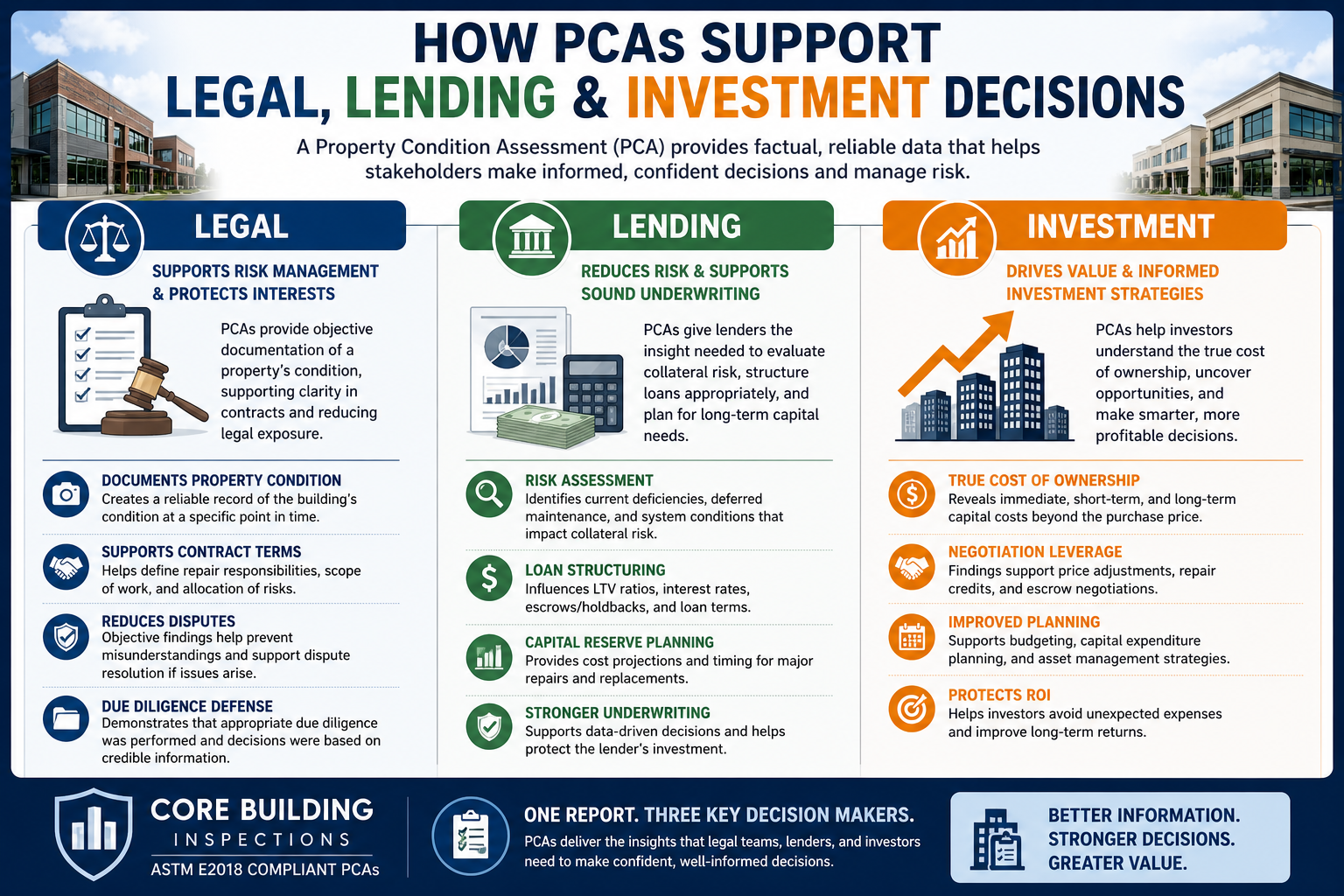

How Lenders Use PCA Reports

For commercial lenders, the PCA is a fundamental underwriting document. When a loan is secured by a physical asset, the condition of that asset is directly relevant to the risk profile of the loan — and the PCA is what quantifies that condition in terms a credit committee can evaluate.

At the most basic level, the PCA tells a lender whether the building securing the loan is in a condition consistent with the value being attributed to it. If major systems are at or near the end of their useful life, if there is significant deferred maintenance, or if immediate repair needs are present, those findings directly inform how the lender structures the transaction. Loan-to-value ratios, reserve requirements, and repair escrow or holdback provisions are all instruments a lender can deploy in response to PCA findings — and they frequently do.

The capital reserve table included in a ASTM-compliant PCA is particularly useful to lenders because it projects capital expenditure requirements over the loan term on a system-by-system basis. A lender evaluating a ten-year loan on a building with an HVAC system that has two years of remaining useful life needs to know that. The PCA provides that visibility in a format that supports loan committee review and ongoing asset monitoring.

In the NJ/PA market specifically, lenders are working with a significant volume of older commercial assets — properties built in the 1960s, 70s, and 80s that may have deferred major system replacements through multiple ownership cycles. The PCA surfaces what those years of deferred maintenance actually look like on a cost basis, which is information no appraisal alone can provide.

How Investors Use PCA Reports

For the investor or buyer, the PCA is the document that closes the gap between the purchase price and the true cost of ownership. The sticker price on a commercial property tells you what the seller wants. The PCA tells you what you are actually buying.

Immediate repair costs, near-term capital needs, and long-term replacement schedules identified in the assessment all factor into the real acquisition cost of an asset. An investor who skips the PCA or accepts a limited-scope inspection in lieu of a full ASTM-compliant assessment is making a financial decision without complete information — and in a market like New Jersey or Philadelphia, where older properties routinely carry concealed deferred maintenance, that is a significant exposure.

PCA findings also create negotiating leverage that buyers would otherwise not have. When a report identifies a roof system at the end of its useful life, a water heater that is decades beyond its expected service life, or an electrical panel with documented safety deficiencies, those findings become the basis for purchase price adjustments, repair credits, or escrow agreements that shift the cost burden appropriately. I have seen PCA findings change the economics of a transaction substantially — not because the building had hidden catastrophic defects, but because no one had formally documented the accumulated deferred maintenance that had been building up for years.

Beyond the transaction itself, investors use PCA data for long-term asset management planning. Capital expenditure forecasting, hold-versus-sell analysis, and ROI modeling all benefit from the system-level cost projections the assessment provides.

How Legal Teams Use PCA Reports

The legal dimension of the PCA is often underappreciated, but it is significant. At its most fundamental level, the PCA creates a documented record of the property’s physical condition at a specific point in time — the date of inspection. That documentation has value in transaction contexts, lease negotiations, and dispute resolution scenarios where the condition of the building at a particular moment is relevant.

In contract structuring, PCA findings help define the boundary between seller obligations and buyer assumptions. When a report identifies specific deficiencies, those findings become the factual basis for negotiating who is responsible for what — whether through repair obligations, price adjustments, or the terms of an as-is agreement. The clarity that a well-executed PCA brings to these conversations reduces ambiguity and, with it, the potential for post-closing disputes.

Perhaps most importantly, the PCA serves as evidence that proper due diligence was performed. In the event of a legal challenge — whether from a lender, a subsequent buyer, or a regulatory body — a party that commissioned and acted on a compliant ASTM PCA is in a fundamentally stronger position than one that did not. The report demonstrates that physical risks were identified, evaluated, and incorporated into the decision-making process. That demonstration of professional due diligence is a meaningful form of legal protection.

Why the NJ/PA Market Makes PCAs Especially Important

The New Jersey and Greater Philadelphia commercial real estate market presents a specific set of conditions that elevate the importance of a rigorous PCA. The regional building stock skews older, with a substantial portion of commercial inventory dating from the postwar era through the early 1980s. These buildings carry the accumulated maintenance history — and deferred maintenance — of multiple decades and multiple ownership transitions.

Seasonal weather in the region is also a significant factor. Freeze-thaw cycling puts sustained stress on masonry, roofing, and site improvements. Coastal and near-coastal exposure in parts of New Jersey introduces moisture and salt air conditions that accelerate the deterioration of building envelopes and mechanical systems. These are not abstract concerns — they show up in the field on virtually every inspection I perform in this region, and they translate directly into capital costs that a buyer or lender needs to understand before closing.

The transaction environment in NJ and PA also tends to be complex, with layered due diligence requirements, active lender scrutiny, and legal teams that expect documentation to be in order. A PCA that is fully compliant with ASTM E2018-15, produced by a practitioner with direct regional experience, provides the credibility and substance those environments demand.

The Cross-Functional Value of a Single Report

What distinguishes the PCA from most other due diligence documents is the breadth of its utility. A single well-executed assessment simultaneously serves the lender’s underwriting process, the investor’s financial planning, and the legal team’s risk allocation and documentation needs. Each of those parties is evaluating the same asset through a different lens, and the PCA provides the foundational data that informs all three perspectives.

That is not true of most reports produced in a commercial transaction. The appraisal tells you value. The environmental Phase I tells you about recognized environmental conditions. The PCA tells you the physical condition of the asset, what it will cost to maintain and repair it, and where the risks live — in a format that every party at the table can use.

Putting It to Work in Your Transaction

If you are acquiring, financing, or evaluating a commercial property in New Jersey or the Greater Philadelphia metro area, a Property Condition Assessment is not an optional line item in your due diligence budget. It is the document that connects the physical reality of the asset to the financial and legal decisions being made around it.

Core Building Inspections performs ASTM E2018-15 compliant PCAs throughout the NJ/PA region, with direct practitioner experience across a wide range of commercial property types. To discuss your project or schedule an assessment, visit www.corecreinspections.com.