When financing commercial real estate in the Northeast, lenders are not looking for a glossy building overview—they are looking for risk clarity. Understanding what NJ & PA lenders expect from a PCA report is critical for buyers, owners, and brokers who want deals to close smoothly without last-minute surprises, holdbacks, or retrades.

In New Jersey and Pennsylvania, where aging building stock, climate exposure, and legacy construction are common, lenders rely heavily on Property Condition Assessments (PCAs) to validate underwriting assumptions and capital planning.

Why Lenders Rely on PCAs in NJ & PA

Commercial lenders use PCAs as a risk management tool, not a pass/fail inspection. Their goal is to understand:

- Near-term capital exposure

- Long-term replacement risk

- Whether deferred maintenance threatens cash flow

- If physical issues could impair collateral value

In the NJ and Philadelphia metro markets, PCAs are especially important due to older assets, flat roof systems, freeze-thaw cycles, and high replacement costs.

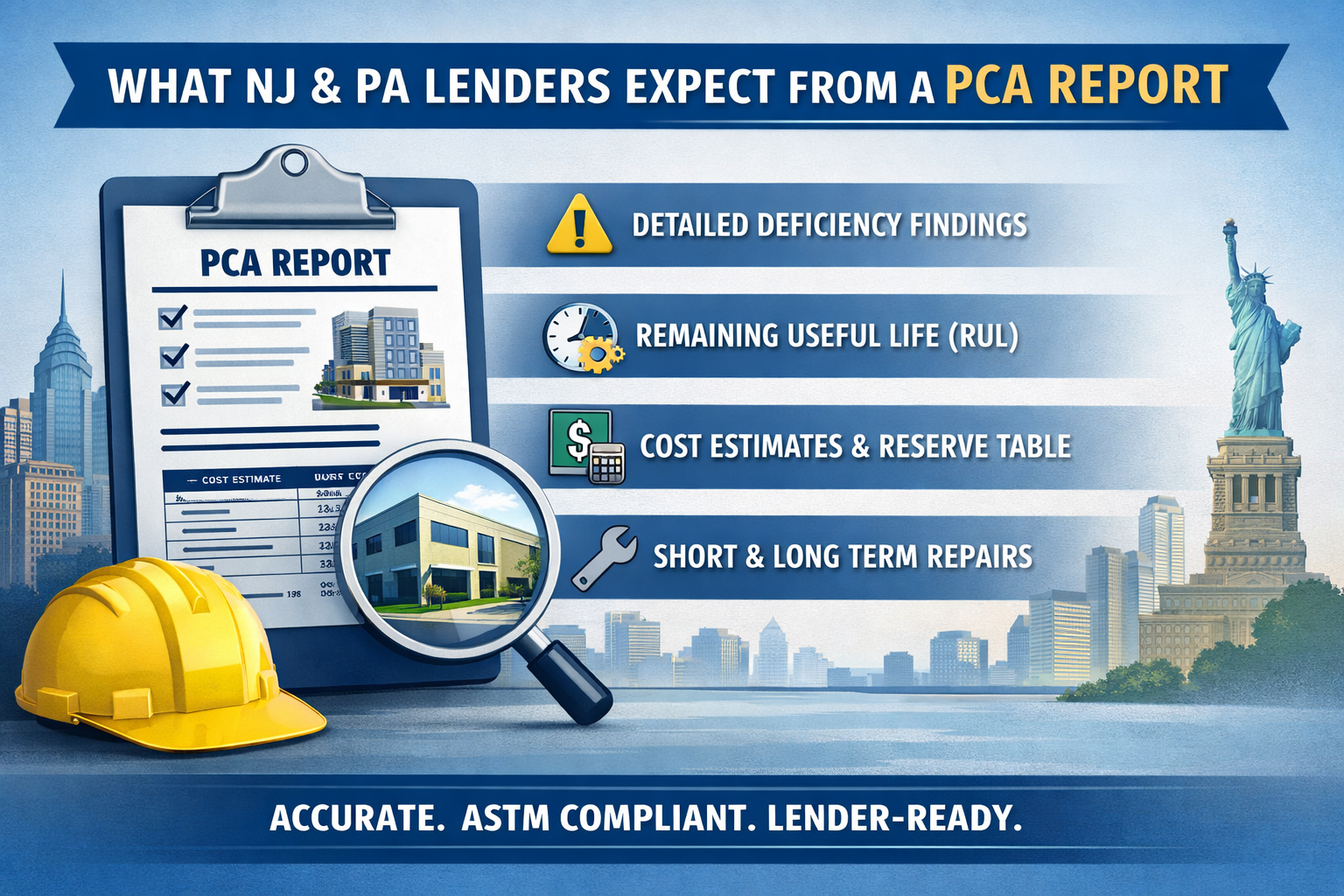

ASTM Compliance Is the Baseline Expectation

First and foremost, NJ & PA lenders expect PCAs to follow ASTM E2018-18 standards (or the current ASTM PCA standard).

This means the report must:

- Follow a standardized structure

- Clearly define scope and limitations

- Identify physical deficiencies (not cosmetic issues)

- Provide remaining useful life (RUL) estimates

- Include capital reserve projections

A PCA that does not align with ASTM guidelines is often flagged for revision or outright rejection by lenders.

Clear Identification of Material Deficiencies

Lenders are primarily concerned with material deficiencies—issues that could reasonably be expected to:

- Affect building operations

- Require significant capital investment

- Impact loan security

Common red flags in NJ & PA PCAs include:

- Roof systems near or beyond end of useful life

- Aging HVAC equipment with limited RUL

- Electrical or life-safety concerns

- Water intrusion or building envelope failures

- Structural issues, even if localized

Lenders expect these items to be clearly documented, not buried in narrative text.

Defensible Remaining Useful Life (RUL) Estimates

One of the most scrutinized sections of a PCA is the RUL analysis. NJ & PA lenders expect RUL estimates to be:

- Realistic and conservative

- Supported by observed condition

- Consistent with regional climate exposure

- Aligned with typical industry benchmarks

For example, a flat roof in New Jersey with visible patching and ponding water is unlikely to be accepted as having a long remaining service life—even if it is not currently leaking.

Short-Term and Long-Term Capital Planning

Lenders do not just want to know what’s wrong—they want to know when money will need to be spent.

A lender-ready PCA includes:

- Immediate repairs (0–1 years)

- Short-term capital needs (1–5 years)

- Long-term replacement planning (6–12 years)

This information feeds directly into underwriting models, reserve requirements, and loan committee discussions.

Realistic Cost Estimates (Not Guesswork)

NJ & PA lenders expect credible, regionally appropriate cost estimates. Costs should reflect:

- Local labor and material pricing

- Market-based replacement assumptions

- Conservative budgeting practices

Underestimated costs can result in:

- Post-closing disputes

- Increased lender scrutiny

- Reduced borrower credibility

Well-supported cost tables increase lender confidence and reduce the likelihood of deal friction.

Transparency About Limitations and Access Issues

Lenders understand that PCAs are non-invasive visual assessments—but they expect transparency.

A strong PCA clearly discloses:

- Areas that were inaccessible

- Information not provided by the seller

- Assumptions used in analysis

- Limitations that could affect conclusions

In dense Philadelphia metro properties, limited access to roofs, tenant spaces, or mechanical rooms is common. Lenders want this documented so risk is properly acknowledged.

Coordination with Other Due Diligence Reports

NJ & PA lenders often review PCAs alongside:

- Phase I Environmental Site Assessments

- ADA Accessibility Surveys

- Appraisals and engineering reports

Consistency across these documents matters. PCA findings that conflict with other reports can trigger additional review or delay closing.

Why Generic PCAs Fail Lender Review

One of the most common issues lenders encounter is PCAs that are:

- Overly generic

- Lacking regional context

- Written by inspectors without CRE experience

- Missing defensible capital planning logic

NJ & PA lenders prefer inspectors who understand local building types, regional climate impacts, and lender underwriting priorities.

How a Lender-Ready PCA Protects the Transaction

A properly prepared PCA helps:

- Reduce loan committee questions

- Support realistic reserve escrows

- Prevent post-closing capital surprises

- Strengthen borrower credibility

- Keep transactions on schedule

In many cases, the quality of the PCA directly influences whether a deal proceeds smoothly—or stalls.

Final Thoughts

Understanding what NJ & PA lenders expect from a PCA report is essential for anyone involved in commercial real estate transactions in the region. Lenders are not looking for perfection—they are looking for clarity, realism, and defensible analysis.

A PCA that meets these expectations becomes a powerful tool for informed decision-making.