If you’ve spent any time in commercial real estate, you’ve probably heard both terms used interchangeably. They’re not the same thing, and confusing them in the middle of a transaction can cost you — either in a deal that falls apart at the lender’s desk or in a property you bought without a full picture of what you were walking into.

The distinction matters most in markets like New Jersey and the Philadelphia metro area, where a significant portion of the commercial inventory is older, has seen multiple ownership transitions, and carries layers of deferred maintenance that don’t announce themselves at a glance.

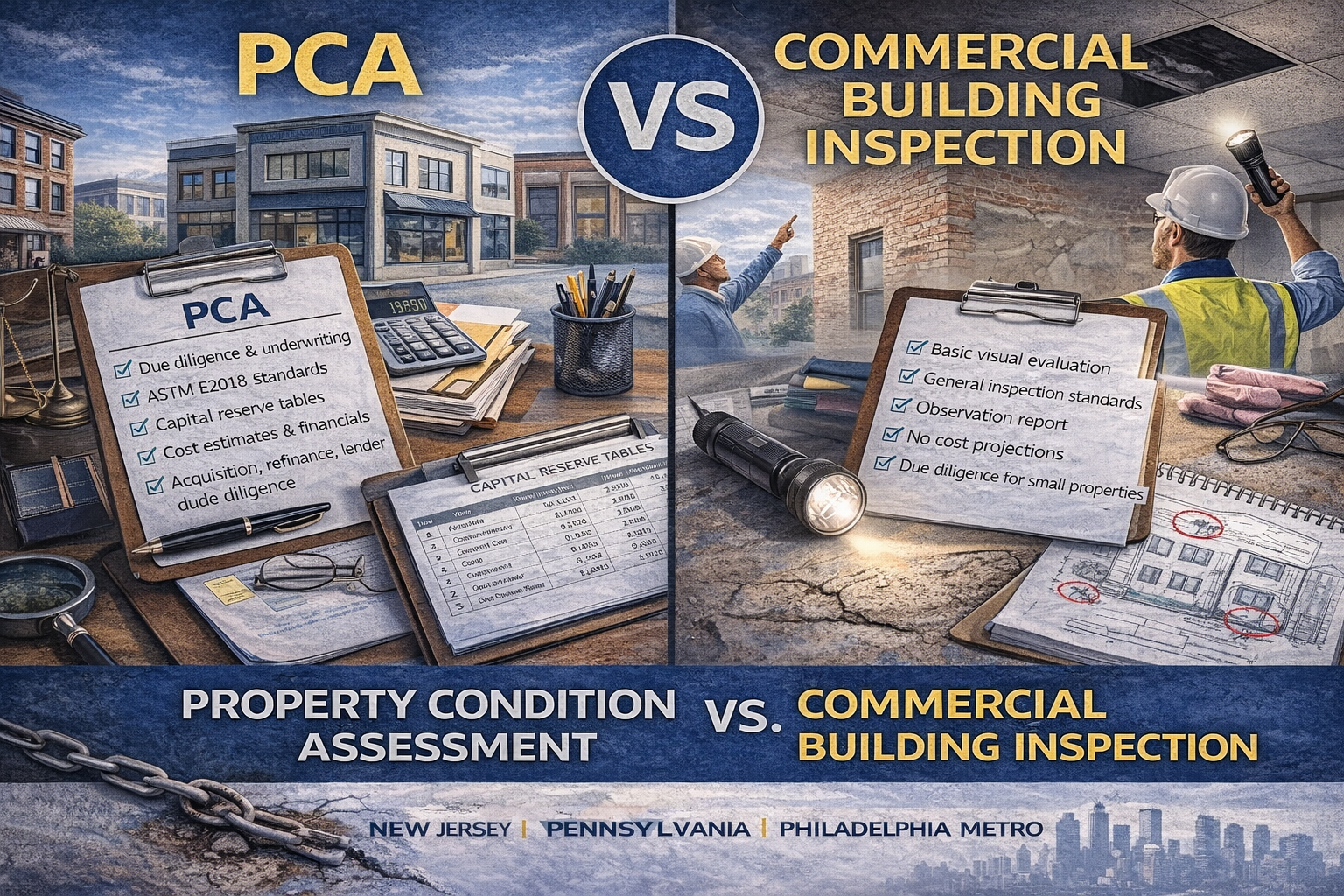

A commercial building inspection is a point-in-time observation. An inspector walks the property, documents visible conditions, flags obvious deficiencies, and delivers a report. It’s useful for getting a general read on a property — particularly in smaller transactions or early-stage evaluations where the buyer just wants to know what they’re dealing with before committing to full due diligence. What it doesn’t do is connect those observations to money. There’s no Remaining Useful Life analysis, no capital reserve projection, no attempt to quantify what the building is going to demand from you over the next decade.

A Property Condition Assessment does all of that. A PCA, conducted in accordance with ASTM E2018, goes well beyond identifying what’s wrong today. It evaluates the physical condition of every major building system — structure, envelope, roof, mechanical, electrical, plumbing — estimates how long each system has left before it needs replacement, and produces a capital planning table that tells you, in dollar terms, what to expect over a defined holding period. That’s the piece lenders care about, and it’s the piece that separates a defensible underwriting document from a general inspection report.

In NJ and PA, lenders require PCAs for a reason. Older building stock means aging roofs, outdated HVAC systems, deferred maintenance on parking and site improvements, and structural modifications that were never properly permitted. A commercial inspection might catch a failing cooling tower or a roof with visible ponding — but it won’t tell you that the boiler has three years of useful life remaining, or that the electrical service will need upgrading before a new tenant can take occupancy. A PCA does.

The practical difference shows up in three places. First, financing: a commercial building inspection won’t satisfy most lender requirements. If you’re acquiring or refinancing a commercial property with institutional debt, a PCA isn’t optional. Second, negotiation: a well-prepared PCA gives you a documented basis for price adjustments or seller concessions — a line-item capital table is a lot harder to argue with than a general inspection report. Third, long-term planning: if you’re holding the asset, you need to know what’s coming. A PCA builds that timeline for you.

A commercial inspection still has a place — pre-purchase gut checks, smaller assets, transactions that don’t involve institutional financing, or early-stage screening before committing to the cost of a full PCA. It’s a valid tool. It’s just not a substitute for the real thing when real money is on the line.

If you’re evaluating a commercial property in New Jersey or the Philadelphia metro area and need a PCA that will hold up with lenders and serve as a legitimate planning document, Core Building Inspections delivers ASTM-compliant reports built for exactly that purpose. Reach out at Core Building Inspections to discuss your property.