There’s a calculation some commercial real estate buyers make during due diligence: the PCA is an added expense, the deal looks clean, and the timeline is tight. So they skip it. It’s a decision I’ve seen backfire in ways that are almost always more expensive — and more avoidable — than the inspection would have been.

A Property Condition Assessment isn’t a formality. It’s a physical audit of what you’re actually buying. And in older markets like New Jersey and the Philadelphia metro area, where building stock runs older and winters run hard, what you don’t know before closing can quietly define your returns for years.

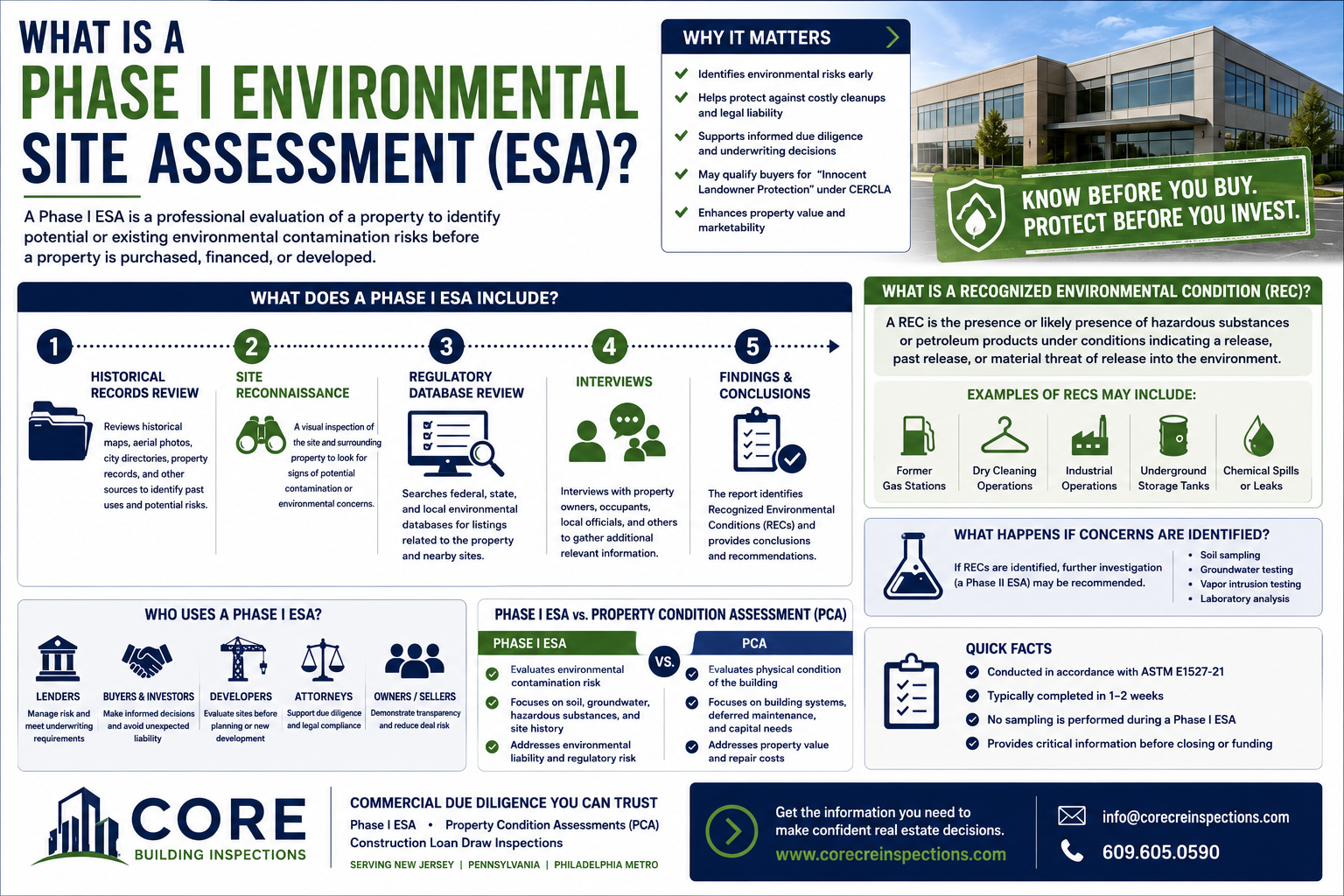

What a PCA Actually Does

A Property Condition Assessment, conducted in accordance with ASTM E2018, is a comprehensive evaluation of a commercial property’s physical condition performed by a qualified inspector before the transaction closes. It documents existing deficiencies, deferred maintenance, estimated remaining useful life of major systems, and projected capital expenditure needs over a defined planning horizon — typically one and ten years out.

The report gives buyers, lenders, and investors an objective baseline of what they’re acquiring. Without it, that baseline doesn’t exist.

The Real Cost of Skipping One

Roof Replacement You Weren’t Expecting

Roof systems are among the most expensive line items in any commercial building. A flat EPDM membrane that looks intact from the ground may be holding water in failed seams, sitting on saturated insulation, or running years past its useful life. On a small strip center, replacement can run well into six figures. On a larger industrial or retail asset, that number climbs quickly. A PCA catches these conditions before closing — when you still have options.

HVAC Systems Near the End of the Line

Rooftop units, air handling equipment, and packaged systems don’t announce failure in advance. They run until they don’t. A building with three aging RTUs, each deferred on maintenance and running on borrowed time, represents a capital exposure most buyers wouldn’t accept if they knew it existed. A PCA identifies these units, estimates their remaining useful life, and puts a number on what replacement will cost. That’s information you need before you sign.

Deferred Maintenance That Compounds Quietly

One cracked parking lot section isn’t a problem. Cracked pavement, failing drainage, spalled concrete at the loading dock, deteriorated exterior caulking, and an aging electrical panel — all in the same building — is a different conversation. Deferred maintenance rarely shows up alone. A PCA surfaces these items together, so you’re looking at the actual capital picture rather than a curated list of what’s visible on a walkthrough.

Negotiating Power You Give Away

Documented deficiencies are leverage. A PCA report gives you objective, third-party evidence to bring back to the table — whether that’s a price reduction, a repair credit, or an escrow holdback. Buyers who skip the PCA walk into that negotiation empty-handed, or they don’t have the conversation at all. Either way, they’re leaving money on the table.

Lender Requirements and Reserve Shortfalls

Most commercial lenders require a PCA as part of the underwriting process, and for good reason. If a property has significant deferred maintenance or systems approaching end-of-life, lenders use that information to set capital reserve requirements. When issues surface after closing instead of before, the reserves are often set too low, cash flow takes the hit, and asset performance suffers. This is a problem that a proper PCA prevents.

Legal Exposure After the Fact

When significant physical deficiencies surface post-closing, the questions that follow are rarely simple. What did the seller know? What was disclosed? Who’s responsible for what? A PCA establishes a documented record of building condition at the time of the transaction. That documentation has value — not just as a planning tool, but as a record that defines the condition of the asset at a specific point in time.

Why It Matters More in NJ and the Philadelphia Metro Area

This region presents a specific set of challenges that make thorough due diligence more important, not less. Older building stock, freeze-thaw cycling that stresses masonry and flat roof systems year after year, aging mechanical equipment in older retail and industrial properties, and deferred maintenance that accumulates over decades of ownership — these are conditions I encounter regularly on PCAs across New Jersey and the Philadelphia suburbs. They’re also conditions that don’t always announce themselves on a casual walkthrough.

The PCA as a Capital Planning Tool

Beyond identifying deficiencies, a well-executed PCA gives ownership a roadmap. The Immediate Repair Table captures what needs attention now. The Capital Reserve Table lays out what’s coming over the next decade. For an investor underwriting returns, a fund manager evaluating a portfolio acquisition, or a lender assessing collateral risk, that information directly informs the decision. The cost of the inspection is not the cost of the inspection — it’s the cost of knowing what you’re buying.

The Bottom Line

In commercial real estate, the most expensive problems are almost always the ones discovered after the keys have changed hands. A Property Condition Assessment doesn’t eliminate risk — no single piece of due diligence does — but it replaces unknowns with documented facts, and that’s what sound investment decisions are built on.

If you’re purchasing or refinancing a commercial property in New Jersey or the Philadelphia metro area, schedule a Property Condition Assessment with Core Building Inspections. Our ASTM E2018-compliant PCA reports give buyers, lenders, and investors an accurate picture of physical condition before the transaction closes.