When a commercial lender underwrites a loan, they’re not taking your word for the building’s condition. They’re commissioning an independent physical evaluation of the collateral — and the findings in that report directly shape how the loan gets structured, what reserves get required, and in some cases, whether the deal closes at all.

That evaluation is the Property Condition Assessment. Understanding what lenders are actually looking for in a PCA helps buyers, investors, and brokers navigate the process with fewer surprises on the back end.

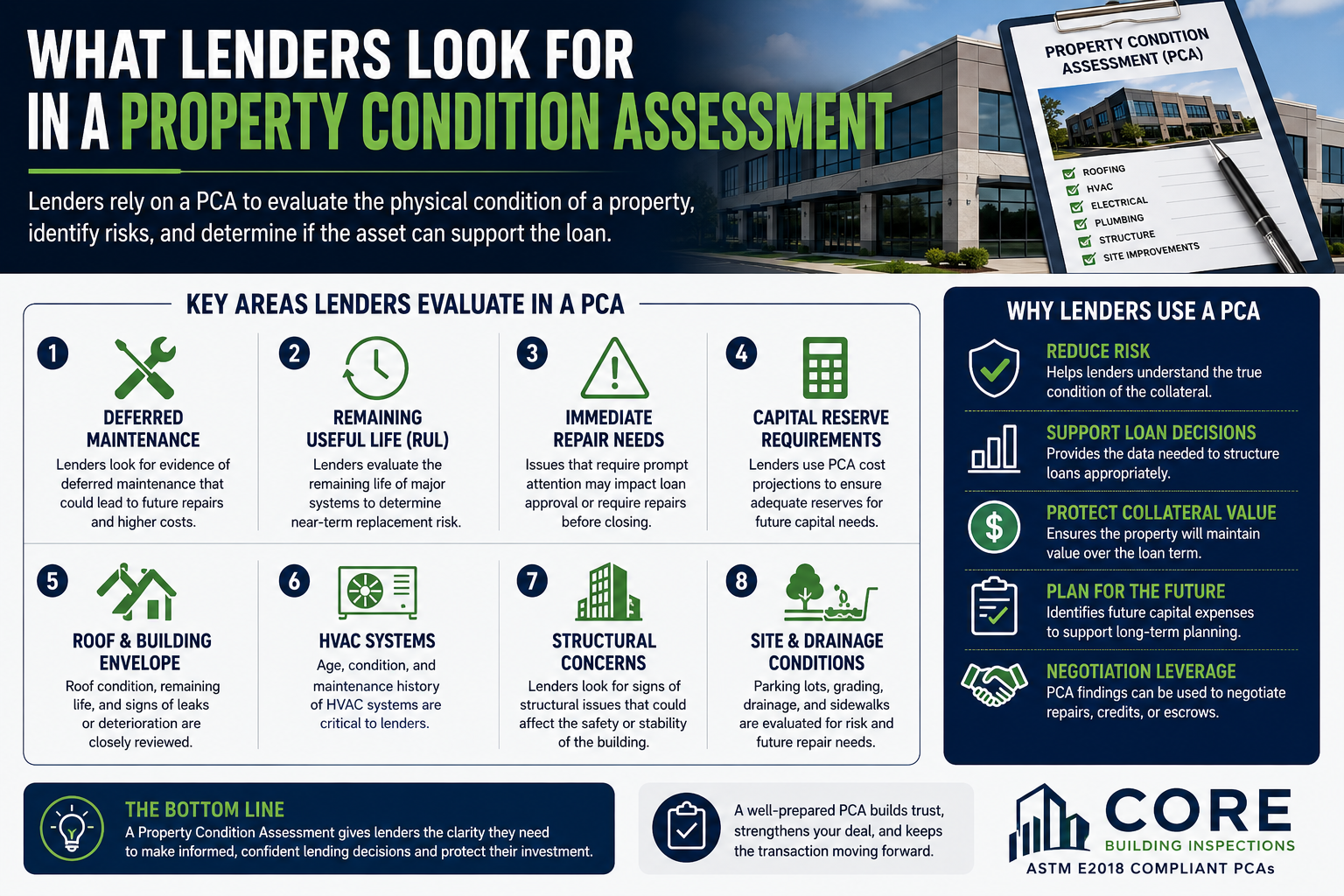

Why Lenders Require a PCA in the First Place

The loan isn’t just secured by the borrower’s creditworthiness. It’s secured by the building. If that building has a roof that’s five years past its useful life, HVAC equipment that’s been deferred on maintenance for a decade, or structural issues that haven’t been addressed, the collateral supporting that loan is worth less than the purchase price suggests.

A PCA conducted in accordance with ASTM E2018 gives the lender an objective, third-party baseline of physical condition. It answers the questions underwriters are trying to answer: Is this building financially viable? Are major repairs imminent? Will deferred maintenance hit cash flow before the loan stabilizes? What capital reserves will ownership actually need?

The report either supports the loan as structured or it doesn’t. Knowing which before closing is better for everyone at the table.

What Lenders Are Looking at in the Report

Deferred Maintenance

This is usually the first thing a lender’s asset manager or credit officer looks for. Deferred maintenance — roof leaks that have been patched repeatedly, parking lots that are past their seal coat and crack fill window, HVAC units running without service records, water intrusion at the building envelope — signals ownership practices and near-term capital exposure simultaneously. A property with significant deferred maintenance is a property that’s been running on borrowed time, and lenders read it that way.

Remaining Useful Life of Major Systems

Lenders don’t just want to know whether systems are functional today. They want to know how much runway is left. The PCA’s RUL estimates for roof systems, HVAC equipment, boilers, water heaters, and electrical infrastructure tell the lender where the capital demands are coming from and when. If three rooftop units are sitting at two to four years of remaining useful life on a ten-year loan, that’s a conversation the lender needs to have before funding — not after.

Systems approaching end-of-life frequently trigger reserve escrow requirements, repair holdbacks, or adjusted loan terms. The PCA is what puts those conversations on the table early enough to structure around them.

Immediate Repair Needs

The Immediate Repair Table in a PCA report identifies conditions that require attention now — active roof leaks, unsafe electrical conditions, structural deficiencies, drainage failures that are causing ongoing damage. These items carry a different weight than long-term capital planning items. They can affect loan approval, push closing timelines, or require completion prior to funding as a loan condition. Lenders treat them accordingly.

Capital Reserve Projections

The ten-year capital reserve table is how lenders evaluate long-term ownership risk. It estimates the timing and cost of major system replacements and significant repairs over the loan term. For underwriting purposes, this informs whether the borrower’s projected cash flow can absorb those expenditures, whether reserves need to be established at closing, and whether the asset’s performance trajectory makes sense against the loan structure. A property with heavy capital requirements in years three through six of a seven-year loan looks very different from one with a clean capital picture through maturity.

Roof and Building Envelope

Roof systems are scrutinized more heavily in a PCA than almost any other component, and lenders know why. A failed roof means water intrusion, and water intrusion means interior damage, mold exposure, tenant disruption, and insurance complications — all of which erode collateral value. Lenders look at remaining roof life, evidence of active or historic leaks, drainage performance, and the quality of any prior repairs. In New Jersey and the Philadelphia metro area, freeze-thaw cycling and heavy seasonal precipitation accelerate deterioration on flat roof systems specifically, and experienced lenders in this market know it.

HVAC Performance and Age

Commercial HVAC systems are capital-intensive and the deferred maintenance risk is high. Lenders look for aging rooftop units, lack of documented service history, systems running outside their design parameters, and equipment that’s functionally obsolete even if it’s still technically operational. Systems in these conditions frequently trigger reserve requirements. For older properties in the NJ/PA region — where mechanical systems often haven’t been touched since the last ownership transition — this is a common pressure point in underwriting.

Structural Conditions

Structural deficiencies are among the highest-risk findings in a PCA from a lending standpoint. Foundation settlement, structural cracking, framing issues, and signs of movement or instability introduce uncertainty that standard reserve requirements can’t easily address. Findings in this category frequently require follow-on evaluation by a structural engineer before the lender will proceed. The PCA surfaces the condition; the engineer quantifies the risk.

Site and Drainage

Site conditions are easy to overlook in a due diligence process focused on the building itself, but lenders pay attention to them. Deteriorated parking lots, poor grading, water ponding near the foundation, and sidewalk trip hazards all represent future capital exposure and potential liability. In our region, where freeze-thaw cycles work on pavement year after year, asphalt and concrete site conditions deteriorate faster than in more temperate markets — and the repair costs reflect it.

Why This Matters Specifically in the NJ and Philadelphia Metro Market

The commercial building stock across New Jersey and the Philadelphia suburbs skews older. A significant portion of what trades in this market was built in the 1960s through 1980s, which means original mechanical systems, aging flat roofs, and decades of deferred maintenance cycles are the norm rather than the exception. Lenders active in these markets have seen enough post-closing surprises to take PCA findings seriously. A PCA that’s thorough enough to surface what’s actually there — not just what’s visible on a walkthrough — is what gives underwriters confidence in the collateral they’re securing.

The PCA as a Lending Instrument

For a lender, a Property Condition Assessment is a risk management document as much as it is a physical inspection report. It helps structure the loan appropriately, establish reserves at the right level, and protect collateral value over the life of the financing. A report that’s vague, incomplete, or conducted by an inspector who doesn’t understand commercial building systems creates exactly the kind of ambiguity lenders are trying to eliminate.

The better the PCA, the cleaner the underwriting. And the cleaner the underwriting, the fewer problems surface at the wrong time.

If you’re financing or acquiring a commercial property in New Jersey or the Philadelphia metro area, schedule a Property Condition Assessment with Core Building Inspections. Our ASTM E2018-compliant reports give lenders the physical condition documentation they need to underwrite with confidence.