When financing a commercial property, lenders are not just evaluating the borrower—they are evaluating the asset itself. One of the most important tools used in this process is the property condition assessment (PCA). Understanding how PCAs influence loan terms, holdbacks, and escrows is critical for buyers, investors, and brokers navigating commercial real estate transactions.

A PCA provides lenders with a clear picture of a building’s physical condition, helping them structure loans in a way that manages risk and protects their investment.

What Is a Property Condition Assessment (PCA)?

A property condition assessment (PCA) is a comprehensive evaluation of a commercial property’s physical condition, typically performed in accordance with ASTM E2018.

A PCA identifies:

- Physical deficiencies

- Deferred maintenance

- Remaining useful life (RUL)

- Capital expenditure requirements

This information is used by lenders to determine how much risk is associated with the property.

Why Lenders Rely on PCAs

Lenders use PCA reports as a key component of their underwriting process.

The report helps answer critical questions:

- Will the property require major repairs in the near term?

- Are there systems at or near end-of-life?

- Are there safety or code-related concerns?

- How much capital should be reserved for future repairs?

The answers to these questions directly impact how the loan is structured.

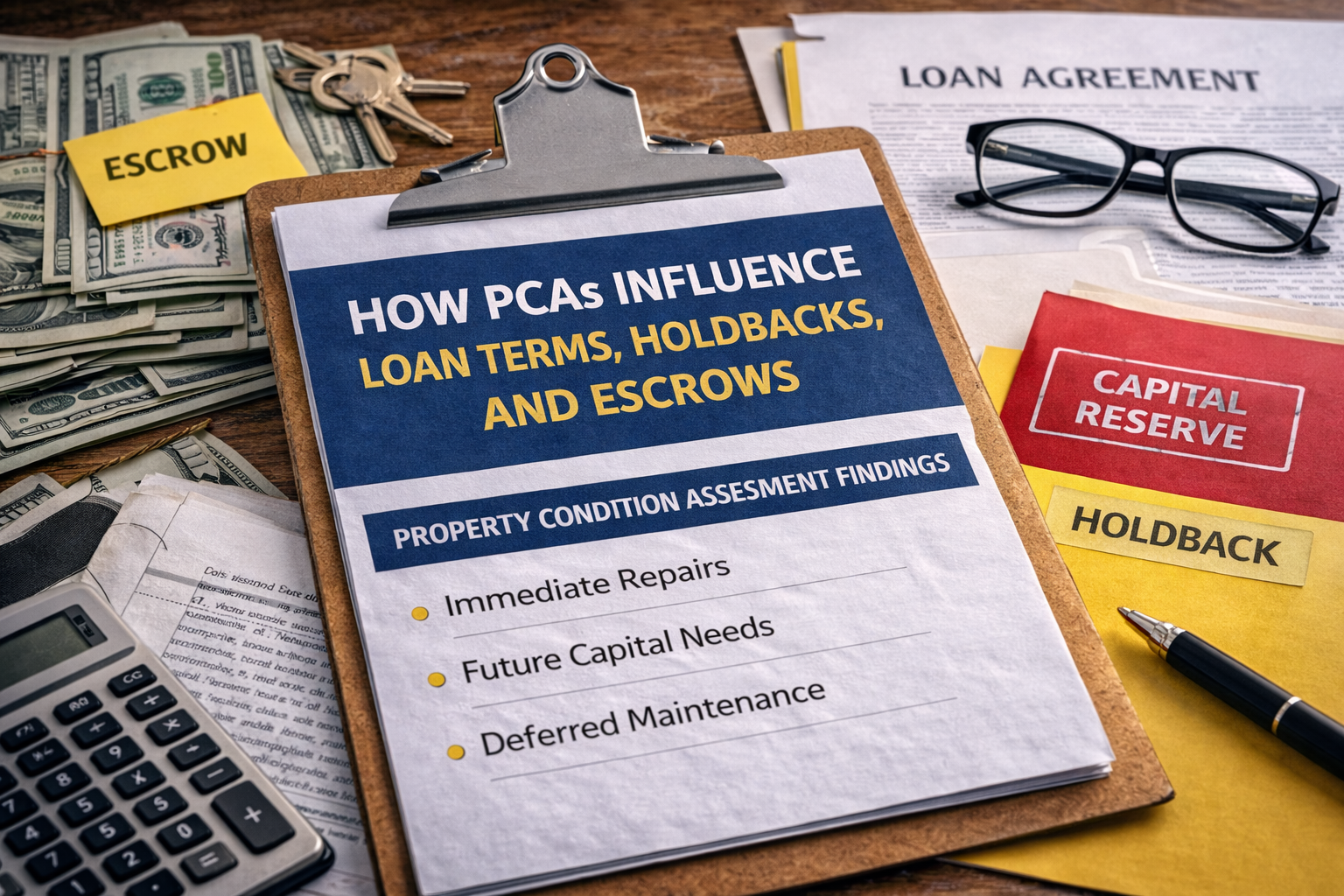

How PCAs Influence Loan Terms

1. Loan Amount and Risk Assessment

If a PCA identifies significant deferred maintenance or upcoming capital expenditures, lenders may adjust:

- Loan-to-value (LTV) ratios

- Loan amount

- Interest rates

Higher risk properties may result in more conservative loan terms.

2. Repair Holdbacks (Escrow for Immediate Repairs)

When a PCA identifies immediate repairs, lenders often require a repair holdback.

A repair holdback:

- Sets aside a portion of loan proceeds

- Ensures that critical repairs are completed after closing

- Protects the lender from asset deterioration

Common triggers include:

- Roof leaks

- Safety hazards

- HVAC systems not functioning properly

3. Capital Reserve Escrows

For longer-term capital needs, lenders may require capital reserve escrows.

These are funds set aside to cover future repairs such as:

- Roof replacement

- HVAC system upgrades

- Parking lot resurfacing

The PCA’s capital reserve table is often used to determine the amount of these reserves.

4. Deferred Maintenance Adjustments

If a property has significant deferred maintenance, lenders may:

- Require repairs prior to closing

- Increase reserve requirements

- Adjust loan structure to reflect risk

This ensures that the borrower is prepared to address existing issues.

5. Influence on Loan Approval

In some cases, PCA findings can impact whether a loan is approved at all.

Properties with:

- Severe structural issues

- Major system failures

- Significant environmental concerns (when paired with ESA findings)

may be considered too high-risk without mitigation.

Real-World Examples

In markets like New Jersey and the Philadelphia metro area, PCAs frequently uncover conditions that affect loan terms, such as:

- Aging flat roof systems nearing replacement

- Rooftop HVAC units beyond useful life

- Deteriorated parking lots requiring resurfacing

- Deferred maintenance in older retail or industrial properties

These findings often lead to repair escrows or adjusted loan structures.

Why This Matters for Buyers and Investors

Understanding how PCAs influence loan terms, holdbacks, and escrows allows buyers to:

- Anticipate lender requirements

- Prepare for capital expenditures

- Negotiate more effectively with sellers

- Avoid surprises during underwriting

A PCA is not just an inspection—it is a financial planning tool.

Final Thoughts

The role of a property condition assessment (PCA) in financing extends far beyond identifying deficiencies. It directly influences how lenders structure loans, manage risk, and protect their investment.

By understanding how PCAs impact loan terms, holdbacks, and escrows, buyers and investors can approach commercial real estate transactions with greater confidence and clarity.

If you are financing or acquiring a commercial property in New Jersey or the Philadelphia metro area, schedule a Property Condition Assessment with Core Building Inspections. Our ASTM-compliant PCA reports provide the insights lenders need—and help you navigate the financing process with confidence.